Loan Repayment Terms Drive Down Debt Service

Unpacking the question of whether interest rates or repayment terms drive debt service levels.

Lower interest rates and longer repayment periods make the annual burden of servicing debt easier. This is an intuitive management concept, and it is exactly what we’ve observed over the last several decades in U.S. agriculture.

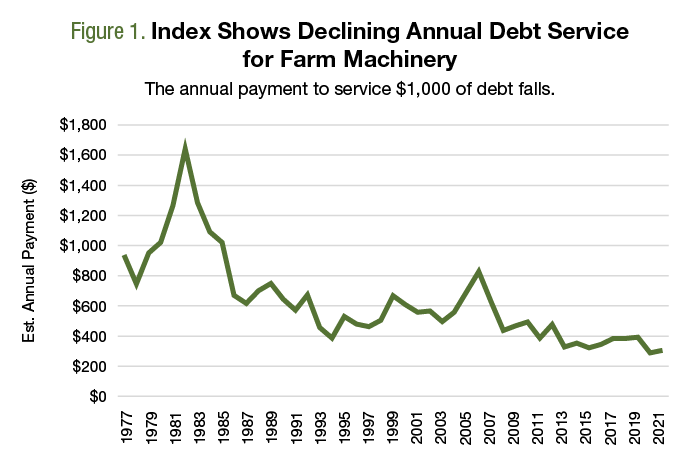

To illustrate this concept, the adjacent graph shows the annual payment required to service $1,000 of farm machinery debt. At the extreme, the Farm Machinery Debt Service Index exceeded $1,600 in 1982 and spent the first half of that decade above $1,000. This occurred because of high interest and extremely short repayment terms. In the early 1980s, the interest rates on farm machinery peaked at 17.9% in 1981, and repayment terms were a low of 8.36 months in 1982. Not ideal times to carry significant amounts of debt.

Since 2013, the index has been below $400. This is significant as the Index previously dipped below $400 in 1994 ($387) and in 2011 ($384). In 2020, the annual data reached an all-time low of $287. For 2021, the Index remains historically low at $305 but turned higher due to shorter repayment terms (43.1 months in 2021 versus 46.7 months in 2020).

Interest Rates Versus Repayment Periods

Between 2020 and 2021, the Index jumped from $287 to $305. Within the underlying data, interest rates fell (4.78% to 4.18%) while repayment periods contracted (46.7 months to 43.1 months). This raised the question: which factor — interest rates or repayment terms — was the driving force behind small annual payments?

In 2000, the Farm Machinery Repayment Index was more than $600. By 2021, however, the index fell by roughly half, to $305. Comparing the terms for those two periods, you’d find that of the roughly $300 decline in the Index, $40 can be attributed to lower interest rates (13%), while $267 (87%) is attributable to longer repayment terms. More specifically, the terms in 2000 were a 9.3% interest rate repaid over 22.4 months, and the terms in 2021 were a 4.18% interest rate repaid over 43.1 months.

Why are repayment terms so important? It’s easy to overlook, but moving from a roughly two-year to a four-year repayment period significantly reduces the annual repayment of principal. The Farm Machinery Index is a bit unique in that the repayment periods have roughly doubled since 2000. While repayment periods have likely extended for other types of farm loans, it seems unlikely that the terms across the sector have doubled for, say, real estate loans.

Wrapping it Up

While much attention in 2022 has focused on rising interest rates, and with good reason, don’t overlook repayment periods. Over the last two decades, farm machinery repayments have nearly doubled, which has also reduced the annual debt service burden.

Low interest rates make extended repayment periods attractive for borrowers. However, higher interest rates may make short repayment periods appealing, given concerns about interest expense. A combination of higher interest rates and a short repayment period would cause the index to jump significantly. In this scenario, a farm with the income to service, say, $50,000 of debt annually would find itself utilizing less debt.

David and Brent are the co-founders of Ag Economic Insights (AEI.ag). Founded in 2014, AEI.ag helps improve producers, lenders, and agribusiness decision-making through 1) the free Weekly Insights blog, 2) the award-winning AEI.ag Presents podcast – featuring Escaping 1980 and Corn Saves America, and 3) the AEI Premium platform, which includes the Ag Forecast Network decision tool. Visit AEI.ag or email David (david@aei.ag) to learn more. Stay curious.

3 Min Read

- Growers’ annual payment on farm machinery debt reached all-time lows over the past decade.

- Interest rates and repayment periods are the two driving factors.

- If loan repayment terms were shortened, annual payments would likely increase.

More Articles About Farm Operations

RECOMMENDED FOR YOU

3 Min Read